Comptroller Kevin Lembo Archive > News

COMPTROLLER LEMBO PROJECTS $82.3-MILLION DEFICITPOINTS TO SOME PROMISING ECONOMIC INDICATORS

Comptroller Kevin Lembo, in his monthly financial projection today, said the state is on track to end Fiscal Year 2017 with a deficit of $82.3 million – although key estimated payment collections data will not be available until mid-January.

Lembo said that January data, budget management and some emerging positive economic indicators could alter future projections.

This projection accounts for the consensus revenue agreed upon by both the Office of Policy and Management (OPM) and the legislature’s non-partisan Office of Fiscal Analysis (OFA) last month that reduced overall General Fund revenue by $49.3 million.

In a letter to Gov. Dannel P. Malloy, Lembo said that his projection is about $14.6 million higher than OPM’s due to his anticipation that there may be higher spending in the adjudicated claims account depending on the timing of settlement payments in the case of SEBAC vs. Rowland.

Lembo noted that there are several factors that could alter this projected deficit (which amounts to less than one half of one percent of net budgeted expenditures) - including continued active budget management to eliminate the shortfall. Lembo also said that, as recent history proves, the largest months for estimated income tax collections are December and January. - which means that key information about this fiscal year’s revenue performance will not be available until about the third week in January.

“It is important to note that the estimated payment component of the tax typically realizes its largest collections during December and January,” Lembo said. By the third week in January, a more reliable trend for this tax component will be apparent. In addition, the payroll-driven withholding component of the income tax historically experiences its strongest receipts between December and March.”

Below is a chart that shows the rate of estimated income tax collections by month for the last two fiscal years (15 and 16).

Lembo projected that net spending will be $59.1 million over budget and, as he has noted in previous months, OPM is relying on a savings target of $203.3 million that is not historically high, but follows successive years of cost cutting, which could make it difficult to achieve.

“To realize no growth in actual year-over-year outlays is a considerable management challenge that will require the skillful efforts of all agencies and branches of government,” Lembo said. And while personal services costs (General Fund payroll costs) have notably declined during the first months of Fiscal Year 2017, “the rate of decline may not be sufficient to realize the large lapse goal.”

Lembo said that there are notable positive economic indicators that are worth highlighting – and may be promising signs going forward. He pointed to some of the latest economic indicators from federal and state Departments of Labor and other sources that show:

• In Fiscal Year 2016 the withholding portion of the income tax increased 3.4 percent from the prior fiscal year. Through October of Fiscal Year 2017, adjusting for accrual differentials, the year-to-date withholding receipts were 1.5 percent above last fiscal year. However, last fiscal year had two additional large deposit days through October. Adjusting for those extra deposit dates the withholding trend is running slightly above last fiscal year.

• Preliminary Connecticut nonfarm job estimates from the business

establishment survey administered by the US Bureau of Labor Statistics (BLS)

show the state lost 7,200 payroll jobs in October 2016 to a level of 1,676,400,

seasonally adjusted. September's originally released job decline of 5,200 was

revised down further to a loss of 6,600.

• It should be noted that while the establishment survey has been showing

deterioration in the Connecticut job market over the past several months, the

household census survey used to calculate the unemployment rate has been

pointing to job gains. The payroll withholding portion of the income tax is also

not consistent with large job losses in the state. The establishment survey on

job growth is benchmarked annually and adjusted. Connecticut has experienced

some significant adjustments to these statistics in past years.

• Based on the current results of the establishment survey, Connecticut has

recovered 69.0 percent (82,200, about 1,028 jobs per month) of the 119,100

seasonally adjusted jobs lost in the Great Recession (3/08-2/10). The job

recovery is into its 80th month and the state needs an additional 36,900 jobs to

reach an employment expansion. The state's private sector has done somewhat

better, recovering 84.3 percent (94,200, or about 1,178 per month) of the

111,700 private sector jobs lost in that same employment downturn. The

Government supersector has lost 19,400 positions since the recession started in

March 2008; including 12,000 since the state's nonfarm employment recovery began

in February 2010.

• As the state’s employment recovery has progressed, an increasing number of job

sectors have posted employment gains.

• U.S. employment has been advancing at a rate of 1.7 percent over the

12-month period ending in October; Connecticut’s employment growth was 0.2

percent.

• Connecticut’s unemployment rate was 5.1 percent in October; the national

unemployment rate was 4.9 percent. Connecticut’s unemployment rate has continued

to decline from a high of 9.5 percent in October 2010.

• There were 97,900 unemployed job seekers in Connecticut in September. A low of

36,500 unemployed workers was recorded in October of 2000. The number of

unemployed workers hit a recessionary high of 177,200 in December of 2010.

![]()

• Average hourly earnings at $30.86, not seasonally adjusted, were up $1.37, or

4.6 percent, from the October 2015 hourly earnings estimate ($29.49). The

resultant average private sector weekly pay amounted to $1,055.41, up $61.60, or

6.2 percent higher than a year ago.

• This strong level of reported wage growth is not consistent with the slower

growth rates posted in other wage and income data. The reported monthly wage

data comes from the business establishment survey, which is subject to large

year-end adjustments. It is highly unlikely that Connecticut’s hourly and weekly

wages grew more rapidly than the national growth rate that remains below 3

percent.

• Connecticut ranked 20th nationally in income growth for the 2nd quarter of

2016 based on personal income statistics released by the Bureau of Economic

Analysis on September 28. The state’s personal income was growing at an

annualized 4.5-percent rate in the 2nd quarter of the year. This growth rate

exceeds that of the prior year.

• Personal income statistics for third-quarter personal income growth will be released on December 20.

• According to a November 22 release from CT Realtors, Connecticut single-family

residential home sales increased 4.6 percent in October 2016 from the same month

a year earlier. The median sale price also posted an increase of 3.3 percent to

$247,000. This marks the second consecutive month of price increases, and it

reverses a persistent trend of monthly declines in home prices. Townhouse and

condominium sales and prices increased in October with both up 1.7 percent.

• The National Association of Realtors (NAR) reported that October's sales of

existing homes rose 2.0 percent over the month to a seasonally adjusted annual

rate of 5.60 million. That was the strongest pace since February 2007. Sales of

previously owned homes in October were up 5.9 percent from a year earlier. The

gains came despite rising prices and shrinking inventory, a sign housing demand

remains solid as the year comes to a close.

• Home prices have been rising far faster than wage gains. The median price of

an existing home sold in October was $232,200, up 6.0 percent on the year.

First-time home buyers accounted for 33 percent of October sales, according to

NAR, down from 34 percent in September, a figure that matched the highest level

since July 2012. Distressed sales ticked up 1 percentage point to account for 5

percent of all sales.

Consumers

• October retail sales were up a solid 0.8 percent compared to September,

which increased the year-over-year growth rate to 4.3 percent from October a

year ago. September was revised upward as well. The two-month increase was the

largest since the spring of 2014.

• The year-over-year gains were as follows: non-store (internet) up 12.9

percent, health/personal care up 8.3 percent, home improvement up 6.5 percent,

auto dealers up 5.8 percent, restaurants/bars up 4.3 percent. Department stores

continued their downward slide, with sales down 7.3 percent, and consumer

electronics sales continue to decline, down 4 percent, due to primarily to

deflation in those goods.

• The University of Michigan’s confidence index rose to a six-month high in

November. The index posted a reading of 93.8, up from 87.2 in October. The split

was stark between respondents in the month’s survey before and after the Nov. 8

vote, with sentiment rising 8.2 points in the post-election group from the

pre-election cohort. This month’s preliminary index reflected about 390

responses on or before the presidential election, while the final gauge included

an additional 220 interviews after the event.

• The current conditions index, which measures Americans’ perceptions of their

personal finances, rose to a four-month high of 107.3 in November from a

one-year low of 103.2 in the prior month. The gauge of expectations six months

from now gained 8.4 points to 85.2, the biggest jump in four years, from a

two-year low of 76.8 in October.

• According to the Federal Reserve’s November 7 report, consumer credit

increased at a seasonally adjusted annual rate of 7 percent during the 3rd

quarter. Revolving credit increased at an annual rate of 5.25 percent, while

non-revolving credit increased at an annual rate of 7.25 percent. In September,

consumer credit increased at an annual rate of 6.25 percent.

Business and Economic Growth

• According to the November 29 release from the Bureau of Economic Analysis,

GDP in the third quarter of 2016 grew at a 3.2-percent annual rate. That was the

strongest rate of growth in two years and followed second-quarter growth of 1.4

percent.

• The acceleration in real GDP in the third quarter primarily reflected an

upturn in private inventory investment, an acceleration in exports, an upturn in

federal government spending, and smaller decreases in state and local government

spending and residential fixed investment, that were partly offset by a

deceleration in personal consumption spending, an acceleration in imports, and a

deceleration in nonresidential fixed investment.

• The solid increase in GDP lowers the probability of a recession in the near

term.

• Corporate profits also continued rebounding in the third quarter. Profits rose

3.5 percent from the second quarter, which was the third straight quarterly

increase. Compared with a year earlier, after-tax profits rose 5.2 percent in

the 3rd quarter, the first annual increase since late 2014 and the strongest

growth since the 4th quarter of 2012.

• Corporate profits have been constrained in recent years by various forces

including weak global growth, a strong dollar, and slumping commodity prices

that contracted the energy and agriculture sectors. But business earnings have

shown signs of stabilization this year as some of those past pressures have

weakened.

• The Commerce Department reported that durable goods orders in October rose 4.8

percent to a seasonally adjusted $239.4 billion from the prior month. Economists

surveyed by The Wall Street Journal expected a 2.7-percent gain in overall

orders. September’s overall orders were revised to a 0.4-percent gain from a

previously estimated decline.

• Orders for civilian aircraft and parts increased 94.1 percent in October from

September. Nondefense capital goods excluding aircraft - a proxy for overall

business investment - rose 0.4 percent last month, but it is down 4 percent

through October, compared with the first ten months of last year. Measures of

manufacturing activity has been choppy over the past year as a strong dollar

caused U.S. made goods to be comparatively more expensive than imports.

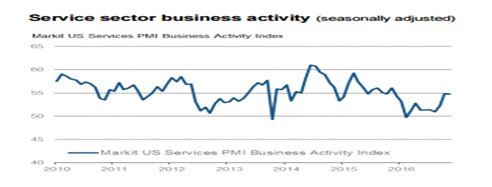

• The service-sector, which is the largest sector of the economy, continued

to post strong growth numbers in November. The Markit Flash U.S. Services PMI

Business Activity Index, adjusted for seasonal influences, was 54.7 in November

compared to a strong October reading of 54.8. The November reading was the

second strongest in more than 12 months. The average reading in the fourth

quarter to date indicates the most rapid upturn in business activity since the

fourth quarter of 2015.

• Service providers indicated an optimistic assessment of their growth outlook

for the coming 12 months. The extent of optimism dropped a bit since October but

continued to be above the post-crisis low seen in June. Survey respondent cited

an expected rebound in the U.S. economic conditions and an associated rise in

client spending as contributing to their positive future outlook.

Stock Market

• Estimated and final income tax payments account for approximately 40

percent of total state income tax receipts. Both the estimated and final

payments had a negative rate of growth in Fiscal Year 2016.

• The first large estimated income tax payment for Fiscal Year 2017 was made in

September. Estimated payments, net of accrual activity, were down 11.4 percent

from last year after the September filings. It should be noted that last fiscal

year, as well as in Fiscal Year 2014, the patterns established in September were

not consistent with the trends during the remainder of the fiscal year. It is

likely that taxpayers adjusted payments in January to address their anticipated

tax liability for the prior calendar year.

• The graphs below show the year-to-date movement in the DOW and the S&P respectively at this writing.